The Financial Sector Conduct Authority (FSCA) has issued its 2020 South Africa FinTech study, which points out that the financial technology market is growing fast. The study uncovered that there are 220 active and operational FinTechs in South Africa and this number is expected to grow as technology adoption increases.

The pace of change and innovation in the FinTech space in South Africa is rapid and on the rise.

It has become even more so in the last year as the effects of the global coronavirus pandemic drove widespread digital adoption and catapulted upstart FinTech firms into the mainstream. This has meant that FinTechs have had to innovate to differentiate themselves and find new and better ways to serve their customers.

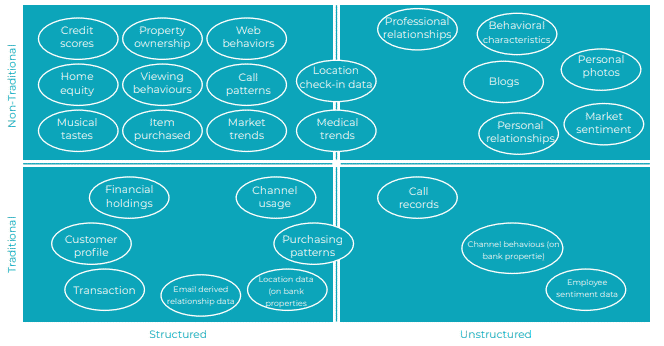

Increasingly, that means using data – and non-traditional or alternative data sourced from

external sources used to supplement core internal organisational data, specifically – to capture value, particularly in the payments, lending and insurance technology (InsurTech) segments.

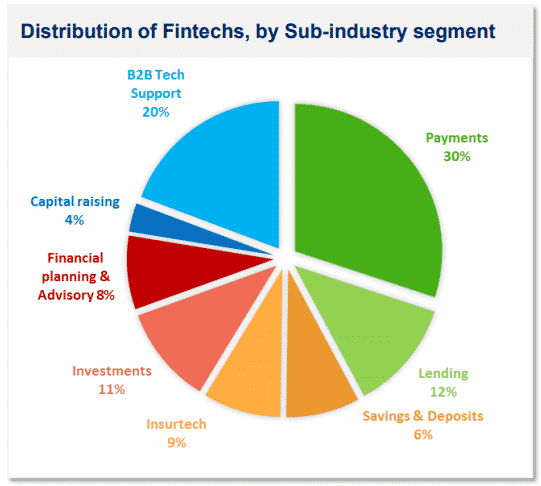

“In payments, FinTechs are using non-traditional data with their transaction data to enhance the mobile payments user experience. Payments is the largest and most mature segment making up 30% of the overall FinTech activity in SA – which is in line with global trends. This is mostly due to the large need for migrant workers in the country to send money to their countries of origin in southern and other parts of sub-Saharan Africa. The second largest segment is B2B Tech such as Blockchain, Robotic Process Automation (RPA) making up 48% of the fintech sector,” says Kagiso Mothibi, Department Head: Fintech at the Financial Sector Conduct Authority (FSCA).

“In lending, FinTechs are building more accurate scorecards, improving customer profiles, making better credit decisions, and managing overall credit risk. InsurTechs are using alternative data to offer policyholders better premiums and to better manage risk.”

The use of non-traditional data is on the rise in South Africa, and comes with both benefits and risks. Key benefits include financial inclusion, personalisation, affordability, and enhanced customer experience.

The main risks are data privacy, data protection, decision bias, fairness and transparency.

However, FinTechs that are able to overcome these challenges by focusing on greater levels of transparency and informed consent, data security, data privacy and the prevention of misuse or biases are proving to unlock these benefits for their customers and ensure that they are sufficiently protected.

Yoco, for example, which is an African payment service provider and technology company that builds tools and services to help small businesses get paid and run their business better, has shown that it can innovate to support customers and enhance their experience.

The company uses data to offer value-added services to customers on their mobile card reader solution. These services include a breakdown of sales, data on forms of payment and tracking of revenue using Yoco’s business intelligence (BI) tool.

Yoco also uses data around a business’s sales history and monthly turnover to offer merchants a cash advance.

“With the introduction of COVID-19, many small businesses were thrown an unexpected curveball. But, for our business model, it extended the trajectory we were on in terms of the move towards cashless. During the period, Yoco also launched new offerings to facilitate the move online by many of our SME’s,” says Hanslo.

“South Africa is mainly a cash economy, but businesses started moving online and with that, it increased the amount of data being processed that now becomes available through the online stores. This introduced greater risks into the system – making mitigation an imperative. From a consumer perspective, greater attention on data protection and governance has been a focus.”

Although just one example, it shows the value data can add to FinTechs and how it acts as a driver of innovation.

4 Comments

Pingback: Acquisitions, E-commerce and the Latest in Australian Fintech - Crowdfund.press

Pingback: Acquisitions, E-commerce and the Newest in Australian Fintech | CryptoLoverz

Pingback: Acquisitions, E-commerce and the Latest in Australian Fintech - Finovate - ई-डिजिटल न्यूज

The implementation of RPA and automation technologies in the financial processes are capable of developing traditional institutions without losing relevance in a rapidly evolving technological landscape and it is indeed to turn real-world benefits. RPA bots can eliminate clerical errors and process claims faster and more efficiently than a human could do. However, cybercrime and fraud have to be tackled with a proper framework for fintech providers in the country. Thank you for sharing this interesting article.